A family trust in Australia is a legal structure that holds business and investment assets separately from your personal name, giving you control over income distribution, asset protection, and wealth transition across generations.

Most family trusts in Australia are technically discretionary trusts. The ATO only treats a trust as a “family trust” when a valid Family Trust Election (FTE) has been made, restricting the family group to a nominated test individual and their relatives under the Income Tax Assessment Act 1997. For the full breakdown of how these terms overlap, read our guide on discretionary trust vs family trust.

One critical point that shapes everything else: a trust does not have a separate legal personality. The trustee holds assets and enters contracts in their own name, on behalf of the trust. This has direct implications for liability, making it one of the key structural decisions SME owners need to get right. Parkview Advisory, a business structuring specialist based in Sydney, works with SME owners on exactly these decisions.

How Does a Family Trust Work

Understanding the mechanics matters because each connects to a commercial decision you will need to make.

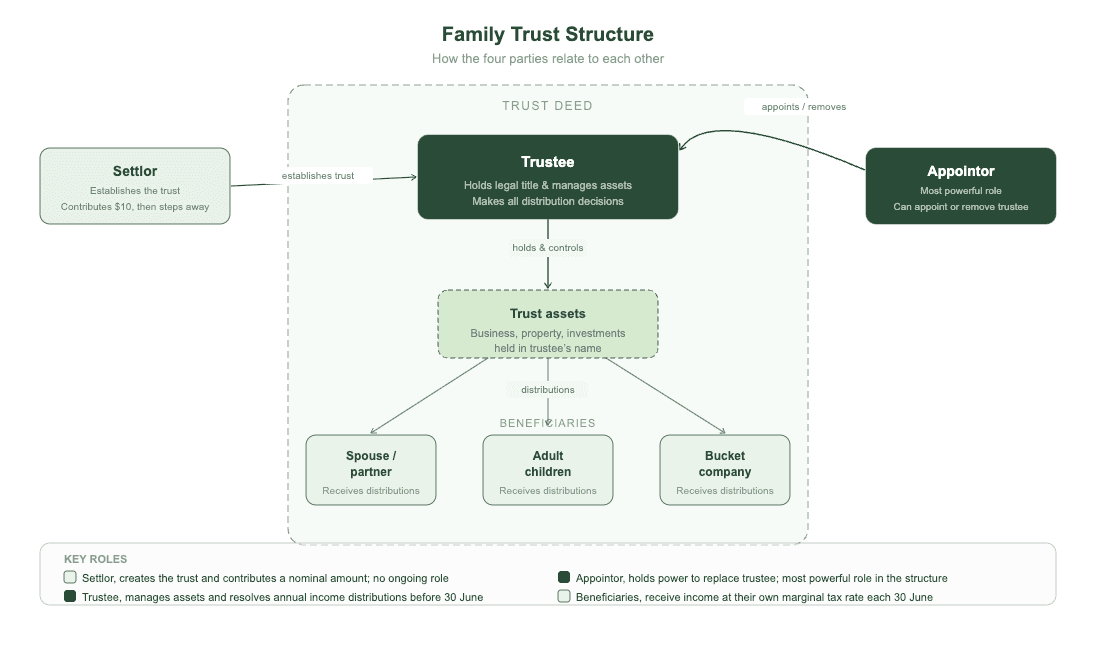

The diagram below shows how the four parties relate to each other and where each sits within the trust deed.

Each of those four roles carries distinct rights and obligations, here is what they mean in practice.

1. The Parties

Four roles sit at the centre of every family trust. The settlor establishes the trust with a nominal contribution and then steps away. The trustee holds legal title to the assets and makes all operational decisions, including distributions. The appointor holds the power to appoint and remove the trustee, making this the most powerful role in the structure. The beneficiaries hold equitable interest in the assets and receive distributions at the trustee's discretion.

2. The Trust Deed

The trust deed governs who can be a beneficiary, what the trustee can and cannot do, and how the trust operates. It is the foundation of the entire structure. Professional drafting avoids costly amendments later, particularly around distribution clauses and beneficiary classes. The deed must be stamped in certain Australian states and territories, with stamp duty obligations varying by jurisdiction.

3. How Distributions Work

Each year, the trustee resolves how to distribute the trust's net income among beneficiaries. Under Division 6 of the ITAA 1936, each beneficiary is assessed on their share of trust net income at their individual marginal tax rate, which is the mechanism that makes income splitting possible.

The timing is non-negotiable. Trustee resolutions must be made before 30 June each income year. Failure to resolve before that date means undistributed income is taxed in the trustee's hands at the top marginal rate of 47 percent. This is not a soft deadline.

Individual vs corporate trustee

Because the trust has no separate legal personality, the trustee bears personal liability for the trust's obligations. If an individual acts as trustee, their personal assets are exposed. A corporate trustee limits that exposure to the assets held within the company. For most SME owners with material business or investment assets, the cost of a corporate trustee is modest relative to the liability protection it provides.

Family Trust Benefits for Australian SME Owners

The advantages of a family trust are best understood through real commercial scenarios, not abstract lists.

1. Income distribution flexibility and tax minimisation

Consider an SME owner earning $300,000 in business profits as a sole trader. At the top marginal rate of 47%, the personal tax bill on that income is approximately $111,232. Now consider the same profits flowing through a family trust, with the trustee distributing $90,000 to a spouse with no other income and $90,000 each to two adult children in lower tax brackets. The total family tax bill can be reduced by $30,000 or more, because each beneficiary is assessed at their own marginal rate rather than the owner bearing the full burden at the top rate.

This is the core income-splitting mechanism under Division 6 of the ITAA 1936. If the trust has made a Family Trust Election, any distribution outside the defined family group triggers Family Trust Distribution Tax (FTDT), levied at the top marginal rate plus Medicare levy. Beneficiary selection is not just a tax planning decision. It is a compliance decision.

For SME owners with profits exceeding personal spending needs, distributions can also flow to a bucket company to cap tax at the corporate rate of 25% (for base rate entities). This pairing keeps surplus profits inside a tax-efficient structure rather than being assessed at individual marginal rates. Parkview Advisory regularly structures these arrangements for Sydney-based SME owners.

2. Asset protection

A family trust separates business risk from personal and family assets. If your business faces legal action, a creditor claim, or a partnership dispute, assets held in the trust are not held in your personal name. They are held by the trustee on behalf of the beneficiaries. According to ASIC data, around 3 in 10 small businesses face some form of commercial dispute within their first five years, making structural separation a practical priority, not just a theoretical one.

For an SME owner operating in a trade business with subcontractor risk, or a professional with indemnity exposure, the trust creates a structural layer between commercial risk and family wealth.

3. Succession and intergenerational wealth

A family trust continues beyond the individual. When a business owner passes away, assets held in a lifetime family trust do not form part of their personal estate in the same way as personally held assets, which can help avoid or defer CGT events on death. The trust structure supports a staged transition to the next generation.

For SME owners thinking longer term, the distinction between a lifetime family trust and a testamentary trust matters. A testamentary trust is established through a will and activated on death, offering specific tax advantages for minor beneficiaries. Both serve succession purposes but suit different planning objectives. Parkview Advisory's business structuring team can help you assess which structure aligns with your succession goals.

When a Family Trust Makes Sense vs When It Does Not

The table below summarises the three archetypes that consistently benefit from a family trust, alongside the three scenarios where a simpler structure is the better fit.

| When a family trust makes sense | When a family trust is not the right fit |

|---|---|

| Profitable business owner with family in lower tax brackets: income splitting reduces total tax across the family unit. | Early-stage business with tax losses: losses are trapped in the trust and cannot be distributed to beneficiaries. |

| Property investor with business exposure: the trust separates investment assets from business creditors. | Sole operator with no dependants: no family members to split income to, so compliance costs outweigh the benefit. |

| Business owner planning succession: the appointor role gives control over a staged handover to the next generation. | Simple, low-income business: administration, annual resolutions, and professional fees may not be justified. |

If you are approaching 30 June, timing matters. Setting up a trust mid-year has practical implications for the first distribution year, and trustee resolutions cannot be backdated. The earlier the structure is in place, the more flexibility you have.

For SME owners who see themselves in these scenarios, the next step is a conversation with Parkview Advisory about whether the structure fits your specific situation.

When a Family Trust is Not the Right Fit

A family trust is a powerful structure, but it is not the right answer for every SME owner. Early-stage businesses with tax losses. Trust losses cannot be distributed to beneficiaries. They are trapped inside the trust and can only offset future trust income. If your business is not yet profitable and you need to carry forward losses, a company structure may serve you better.

The income-splitting benefit depends on having family members in lower tax brackets to distribute to. If you have no spouse, no dependants, and no family members who would benefit from distributions, the compliance cost outweighs the advantage. Our guide on sole trader vs company covers the alternatives.

If your income is modest and your asset protection needs are low, a family trust adds layers of administration and professional fees that may not be justified. The right structure is the one that matches your commercial reality.

How to Create a Family Trust in Australia

If you are looking at how to open a family trust, the setup process involves six steps. Each one has detail behind it, but the sequence is straightforward. Parkview Advisory handles each stage for SME owners across Sydney and nationally.

- Choose the trustee structure: Decide whether an individual or a corporate trustee will hold the trust's assets. For most SME owners with material assets, a corporate trustee is the stronger choice for liability protection.

- Draft the trust deed professionally: The deed is the foundation. A generic template creates long-term problems, including inflexible distribution clauses, missed FTE implications, and potential exposure to Section 100A (the ATO's provision targeting non-genuine trust distributions).

- Settle the trust: The settlor contributes a nominal amount, typically $10, to bring the trust into existence.

- Apply for a TFN and ABN: The trust needs its own Tax File Number and, if carrying on a business, an Australian Business Number.

- Make a Family Trust Election if required: The FTE nominates a test individual and restricts the family group. Once made, distributions outside the family group attract FTDT.

- Stamp the deed where required: Stamp duty obligations vary by state and territory and must be confirmed at establishment.

Getting the deed wrong, or relying on a template that does not reflect your commercial circumstances, is the most common and most expensive mistake in this process. Professional drafting from the start is worth the investment.

Frequently Asked Questions

How much does it cost to set up a family trust in Australia?

The total cost typically ranges from $1,500 to $3,500, depending on whether you use an individual or corporate trustee and the complexity of the deed. A corporate trustee adds ASIC registration fees of around $576, plus the cost of professional deed drafting. Ongoing compliance, including annual tax returns and trustee resolutions, generally costs $1,000 to $2,500 per year. Contact Parkview Advisory for a fixed-fee quote tailored to your structure.

Can I set up a family trust myself?

Technically yes, but it is not advisable for most SME owners. DIY trust deeds are often inflexible, miss critical ATO compliance requirements such as Family Trust Election implications, and can expose the structure to Section 100A risk. The trust deed is the foundation of the entire structure: errors are expensive to fix and can undermine the tax and asset-protection benefits you set the trust up to achieve. Parkview Advisory's business structuring service provides professionally drafted deeds as part of a complete setup.

How long does it take to establish a family trust?

Once the deed is drafted and the trustee structure is confirmed, most trusts can be established within five to ten business days. Applying for a TFN can take an additional two to four weeks via the ATO. If you are approaching 30 June and need the trust in place for the current income year, start the process at least four to six weeks before year end. Book an appointment with Parkview Advisory to confirm your timeline.

Getting the Structure Right Matters

Setting up a family trust in Australia is a structural decision with long-term tax and asset-protection consequences. Deed errors, missed Family Trust Elections, and Section 100A exposure are expensive to unwind and can undermine the very benefits the trust was designed to deliver.

The trust deed, trustee structure, and beneficiary classes need to reflect your commercial reality. They need to work for your business today and adapt as your circumstances change. That requires advisory input at the front end, not just at tax time. Parkview Advisory's business structuring service in Sydney provides end-to-end support from deed drafting to annual compliance.

A well-structured family trust, reviewed regularly and aligned with your business goals, becomes part of your finance function. It supports decision-making on distributions, asset protection, and succession year after year. You may also find our related guides on tax planning strategies and how to minimise tax in Australia useful reading.

Talk to Parkview Advisory about whether a family trust is the right structure for your business.

This article provides general information only and does not constitute financial, tax, or legal advice. The information is current as at the date of publication but may not reflect recent legislative changes. Speak to a qualified adviser at Parkview Advisory or another registered tax professional about your specific circumstances before making any structural decisions.