If you are searching for how to protect your assets from your partner, the most important thing to understand is this: asset protection strategies Australia requires structural prevention that must be in place before a claim arises. Once a creditor sends a letter of demand or a relationship starts to fracture, restructuring is almost always too late. SME owners face a dual threat that most people never consider simultaneously.

Relationship breakdown exposes personal wealth through the Family Court. Business liability exposes it through creditor claims, insolvent trading actions, and contractual disputes. According to the Australian Bureau of Statistics, around 33% of Australian marriages end in divorce, and de facto relationship breakdowns are not tracked separately but are estimated to be similarly prevalent. Most owners only think about protection after one of these threats appears. By then, the window has closed.

The reason is the Bankruptcy Act 1966 (Cth). Transactions entered into within four years of bankruptcy may be voided as uncommercial transactions or transfers to defeat creditors. If you were insolvent at the time of the transfer, that clawback window extends to ten years. The Family Court has its own broad discretion to look through structures and consider trust distributions and control when assessing a party's financial resources. Timing is everything. The structures that protect you are the ones built during calm, not crisis.

How Common SME Structures Leave You Exposed

A sole trader has zero legal separation between personal and business assets, every business debt is a personal debt and every claim against the business is a claim against the family home. A single trading company is better, but not by much. Under the Corporations Act 2001 (Cth), company directors can be held personally liable for insolvent trading under Section 588G. If you continue to incur debts while the company is insolvent, your personal assets are on the table. ASIC data shows that insolvent trading is cited as a contributing factor in approximately 40% of company liquidations that result in director liability actions.

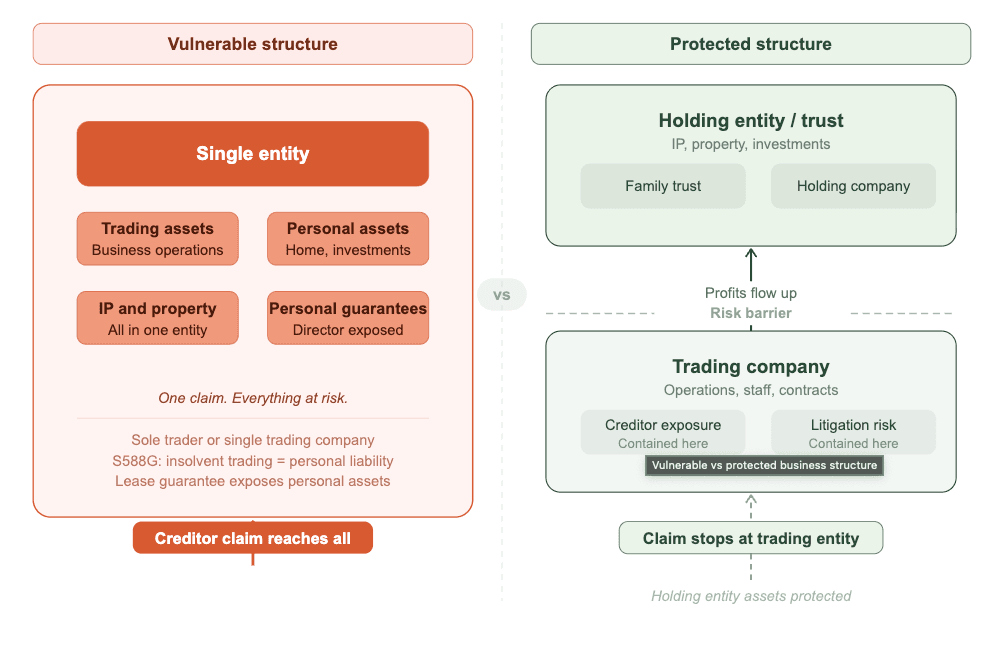

Consider the difference. A vulnerable structure: one company trades, holds assets, employs staff, and the director personally guarantees the lease. A single claim can reach everything. A protected structure separates the trading risk from the asset base. Different assets sit in different legal entities, each with a defined purpose and contained exposure.

The diagram below makes the contrast concrete: on the left, a single entity where one claim reaches everything; on the right, a dual-entity structure where the risk barrier stops a creditor claim before it reaches the holding entity.

That separation between trading risk and asset ownership is the single most important design decision in any asset protection framework.

This concept of structural separation is the foundation of effective asset protection strategies. It is also the starting point for business structuring advisory that actually reduces risk rather than just managing compliance. Legal Aid Queensland's guidance confirms that third-party orders can be made against entities including companies and trusts that hold assets in which a party has a legal or equitable interest. Structure matters, but only if it is done properly.

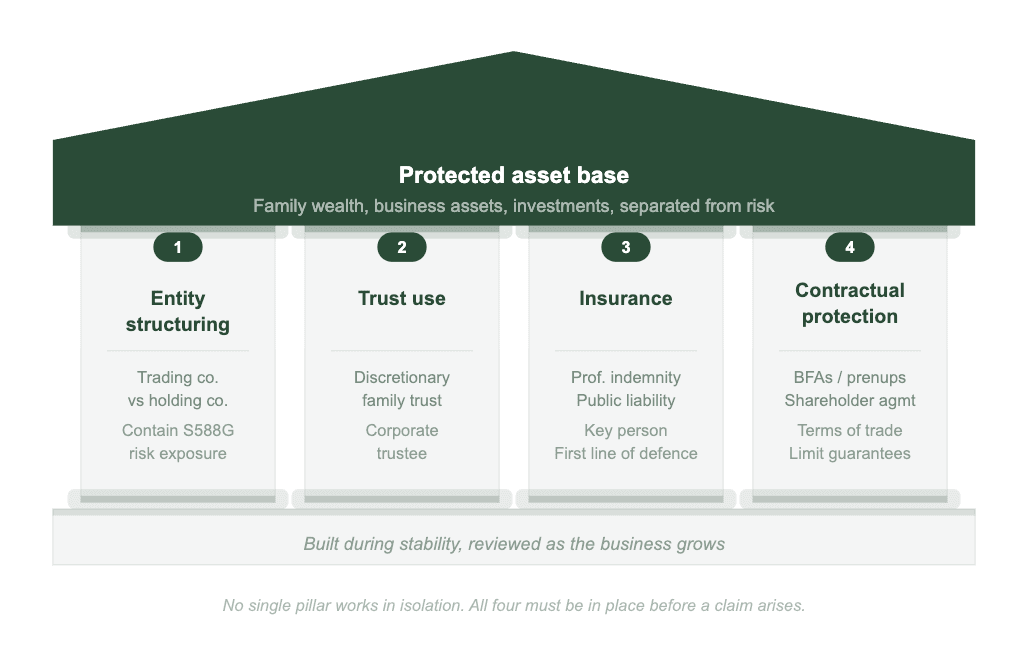

Asset Protection Strategies: The Four Pillars

Asset protection strategies are structural choices made during periods of stability to separate valuable assets from business and personal liability risk, using entity structuring, trusts, insurance, and contractual protection.

The graphic below shows how the four pillars work together: each one addresses a distinct layer of risk, and the protected asset base only holds if all four are standing.

Here is what each pillar covers and how it reduces your exposure.

Effective business asset protection uses four pillars working together. No single tool works in isolation. These are structural choices made during a period of stability, not tactical tricks deployed under pressure. Each pillar addresses both relationship breakdown and business liability risk:

- Entity structuring. Separate the trading entity from the holding entity to contain operational risk.

- Trust use. Discretionary trusts hold non-business assets away from creditor risk.

- Insurance. Professional indemnity, public liability, and key person cover absorb claims before they reach assets.

- Contractual protection. Binding Financial Agreements, terms of trade, and shareholder agreements define and limit exposure.

Pillar 1: Entity Structuring and Dual-Entity Separation

The core technique is separating the trading entity from the holding entity. The trading company takes on operational risk: creditor exposure, litigation, contractual liability. A separate holding entity owns the valuable assets: intellectual property, real property, equipment, investment portfolios.

This is where holding company structures become critical. A holding company sits above the trading entity, receives profits via dividends, and holds assets away from the operational risk zone. The trading company operates lean. The holding company accumulates wealth.

The practical effect is containment. A creditor claim against the trading entity cannot automatically reach assets held in the holding entity. Section 588G personal liability for insolvent trading applies to the trading company's directors, but the assets held in a properly separated holding entity are not directly exposed to this risk. In a relationship breakdown, the property pool becomes more complex to assess, which changes the negotiation dynamics entirely.

Dual-entity separation is not about hiding assets. It is about ensuring that a single point of failure in the business does not cascade into total personal financial loss. Parkview Advisory's business structuring team in Sydney designs dual-entity frameworks as part of every comprehensive asset protection engagement.

Pillar 2: Using an Asset Protection Trust

Discretionary trusts (also called family trusts) can hold non-business assets to isolate them from business creditor risk. Investment portfolios, share holdings, and in some cases the family home can sit within a trust structure. If you need a primer, start with how family trusts work in Australia.

A corporate trustee enhances protection further. When a company acts as trustee rather than an individual, the legal owner of trust assets is separated from any natural person. Explore corporate trustee services if this is relevant to your situation.

Be clear-eyed about the limits. An asset protection trust is not bulletproof against the Family Court. Courts have discretion to consider trust distributions and control when assessing a party's financial resources. Sham trust principles apply if the trust is not genuinely administered. Third-party orders can reach trust assets where a party has a legal or equitable interest. A well-structured, genuinely administered discretionary trust reduces exposure. A poorly structured one creates a false sense of security.

If you are considering this path, setting up a family trust with proper advice from the outset is the difference between protection and paperwork. Parkview Advisory establishes and reviews trust structures for SME owners as part of a complete asset protection framework.

Pillar 3: Insurance as a Structural Layer

Insurance is the first line of defence. Professional indemnity, public liability, and key person insurance absorb claims before they reach business or personal assets. Entity structuring and trusts are the second and third lines. Insurance is the buffer that prevents most claims from ever testing those deeper layers.

Underinsurance is one of the most common asset protection gaps in scaling SMEs. Research from the Insurance Council of Australia indicates that up to 80% of small businesses are underinsured relative to their actual replacement costs and liability exposure. A business that turned over $500,000 three years ago and now turns over $2 million likely has the same policy limits. Insurance should be reviewed annually as the business grows, not renewed on autopilot.

Think of insurance as structural, not transactional. It is a layer in your asset protection structures, not a standalone product.

Pillar 4: Contractual Protection

Binding Financial Agreements (BFAs) are the primary contractual tool for relationship breakdown protection. Under Sections 90B, 90C, and 90D of the Family Law Act (for marriages) and Sections 90UB, 90UC, and 90UD (for de facto relationships), BFAs can be made before, during, or after a relationship. They can quarantine specified assets from a property pool. Both parties must obtain independent legal advice for the agreement to be binding.

De facto partners in most Australian states and territories have the same property settlement rights as married couples under Part VIIIAB of the Family Law Act. This means BFAs are equally relevant whether you are married or not.

Superannuation and BFAs. Superannuation is treated as property in Family Court settlements and can be split via a superannuation splitting order. BFAs can address super entitlements directly, which is important for SME owners whose retirement savings represent a significant proportion of their total wealth. In 2022-23, the average superannuation balance for Australians aged 55-64 was $402,838, making it one of the largest assets in any property settlement.

Every personal guarantee you sign punches a hole in your asset protection structure. Be deliberate about which guarantees you accept and negotiate caps where possible. On the business side, contractual protection also includes terms of trade that limit liability and shareholder agreements that address what happens to equity on relationship breakdown.

How to Protect Your Assets

Pre-relationship and during-relationship structural choices have legitimate roles in protecting assets built before or outside the relationship. Trusts, entity separation, and BFAs are all recognised tools when established genuinely and in advance.

The distinction that matters is timing and intent. Post-separation restructuring almost always fails. Courts treat it as an attempt to defeat a partner's claim, and transfers can be unwound under the Bankruptcy Act 1966. Legitimate planning happens during stability. Improper claw-back attempts happen during crisis. Courts can tell the difference. As covered in Pillar 2, the Family Court has broad discretion to look through structures, so genuine administration of any trust or entity is non-negotiable.

De facto relationships are recognised under the Family Law Act 1975 (Cth) once a couple has lived together on a genuine domestic basis. There is no automatic 50/50 split and no fixed time threshold. De facto partners generally have a two-year time limit to apply for a property settlement after separation.

The asset protection structures that hold up in Australia are the ones built transparently, administered genuinely, and reviewed regularly.

When You Need an Asset Protection Lawyer vs an Accountant

Asset protection lawyers handle documentation: BFAs, trust deeds, shareholder agreements, and litigation when structures are challenged. An asset protection attorney is essential for the legal instruments that give your structure enforceability.

Asset protection accountants play a different role. They design the overall structure and ensure it works commercially and tax-efficiently. Asset protection accountants model the cash flow implications of entity separation, advise on profit extraction strategies between entities, and ensure the structure scales with the business.

Parkview Advisory sits in the strategic structuring role. We architect the overall asset protection framework and coordinate with your legal advisors on documentation. Our asset protection structuring service is advisory-led, not compliance-led. We operate as a full finance function and extension of your business, available for day-to-day decision support, not just year-end lodgements.

The best outcomes come when your accountant and lawyer work from the same structural blueprint. Speak to Parkview Advisory about getting that blueprint in place.

This article provides general information only and does not constitute legal or financial advice. The information is current as at the date of publication and may not reflect recent legislative or case law changes. Seek independent professional advice from a registered legal practitioner and a qualified financial adviser for your specific circumstances.

Frequently Asked Questions

Can I transfer the house to my spouse to protect it?

Generally no, if done to defeat a creditor or partner's claim. Courts can unwind transfers made at undervalue or with intent to defeat claims under the Bankruptcy Act 1966, with clawback windows of four to ten years. Speak to a qualified adviser before making any transfer.

Does a discretionary trust protect against the Family Court?

It can reduce exposure but is not bulletproof. Courts have discretion to consider trust distributions and control when assessing financial resources. Third-party orders can reach trust assets where a party has a legal or equitable interest. A well-administered trust is far stronger than a neglected one.

What is the difference between a BFA and a prenup?

A Binding Financial Agreement (BFA) under Section 90B of the Family Law Act is the Australian legal equivalent of a prenuptial agreement. “Prenup” is informal language borrowed from the US, the correct Australian instrument is a BFA. Unlike a prenup in some jurisdictions, a BFA requires both parties to obtain independent legal advice before signing, and must be documented in writing to be enforceable. BFAs can also be entered into during or after a relationship, not only before it.

What about overseas asset protection structures?

Generally a red flag in Australia. Courts take a dim view of offshore structures designed to defeat claims, and the ATO has extensive information-sharing agreements with foreign jurisdictions. Onshore structures done properly are more effective and far less likely to attract adverse judicial attention.

When is the right time to set up asset protection structures in Australia?

During a period of stability, before any claim or relationship breakdown is on the horizon. The most expensive mistake is waiting until risk is imminent, because clawback provisions mean the structure may be unwound entirely.

The Most Expensive Asset Protection Mistake is Waiting

Asset protection is structural prevention, not litigation response. The structures that work are the ones established during periods of stability, not under pressure. They need ongoing review as the business scales, with monthly reporting and regular strategic meetings to ensure the framework keeps pace with growth.

Relationship breakdown and business liability are both real risks for scaling SME owners. The same structural framework addresses both. The four pillars: entity structuring, trust use, insurance, and contractual protection, work together to contain risk across every dimension of your financial life.

For further reading, see our guides on tax planning strategies, business structuring for SMEs, and how to minimise tax in Australia.

Talk to Parkview Advisory about asset protection structuring that works before you need it.