The most common ATO family trust blunder tax liabilities are now being actively pursued, and the consequences are landing on SME owners who assumed their structures were compliant. The ATO's posture on family trusts has shifted from warnings to active enforcement. If you have been watching the rising search interest in “australia family trust tax reform,” you are not alone.

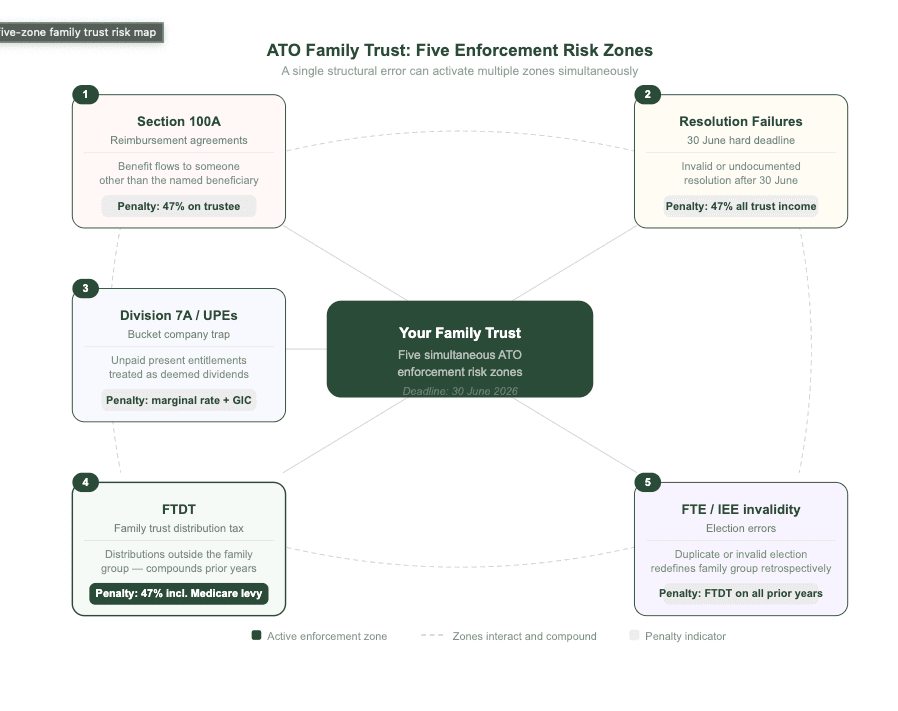

Understanding how family trusts work in Australia is the starting point. But in 2026, understanding the risk landscape is what protects your business. The ATO is pursuing five interconnected risk zones simultaneously: Section 100A reimbursement agreements, Division 7A exposure on unpaid present entitlements (UPEs), Family Trust Distribution Tax (FTDT), invalid or duplicate family trust elections (FTEs), and trustee resolution failures.

These are not isolated compliance items. They overlap. A poorly managed bucket company creates Division 7A exposure. A duplicate FTE triggers FTDT on years of historical distributions. The ATO has also flagged intergenerational wealth transfers and pre-capital gains tax (CGT) asset holdings (assets acquired before 20 September 1985) as high-risk monitoring areas. The 30 June trustee resolution deadline creates a hard action window. The consequences of inaction range from top marginal rate assessments to seven-figure retrospective liabilities.

The diagram below maps all five risk zones and the points where they intersect, a single structural error can activate more than one zone at the same time.

The sections that follow break down each zone in detail, starting with the one the ATO is pursuing most actively right now.

What Recent ATO Rulings Mean for Your Family Trust

The ATO is winning on technical grounds that many business owners assumed were safe. The pattern across recent family trust court rulings is consistent: the ATO is enforcing the letter of the law on elections, distributions, and trust deed compliance, and it is succeeding.

The duplicate FTE case illustrates the scale of exposure. A trust inadvertently made two family trust elections with different test individuals. The second election redefined the family group. Every historical distribution that fell outside that second family group triggered FTDT at 47%. Based on ATO guidance modelling, a duplicate FTE maintained over several years of trust distributions can produce a liability exceeding $13 million. The result accumulates over years of distributions the trustee believed were compliant.

The ATO's own guidance identifies the primary drivers behind increasing FTDT issues: inadequate record keeping, succession planning gaps, intergenerational expansion of businesses, and evolving private group structures. According to ATO compliance data, over 70% of trust reviews that result in amended assessments involve deed deficiencies or election errors. An outdated or poorly drafted trust deed is often the root cause. Parkview Advisory's Sydney-based business structuring team reviews trust deeds as part of every engagement.

There is a General Interest Charge amnesty available for certain FTDT liabilities, but it has specific eligibility conditions and time limits. If you suspect a duplicate or invalid election exists in your structure, the window to act is narrowing.

Section 100A Red Zone Arrangements

Section 100A of the Income Tax Assessment Act 1936 (ITAA 1936) targets trust distributions where the named beneficiary does not genuinely receive the economic benefit. Where the ATO identifies a reimbursement agreement, it can recharacterise the distribution as assessable income of the trustee at 47% including Medicare levy. The ATO's approach is codified in Taxation Ruling TR 2022/4, which sets out when the ordinary family or commercial dealing exemption applies and when it does not.

Example: Section 100A red zone arrangement

A trust distributes $100,000 to an adult child on a low income. On paper, the child is the beneficiary. In reality, the funds are transferred back to the parents or used to pay family expenses. The child never had genuine control of the money. The ATO classifies this as a reimbursement agreement. The full $100,000 is recharacterised as assessable income of the trustee, taxed at 47% including Medicare levy, producing a tax bill of $47,000 on income that was assumed to be tax-efficiently distributed.

The key defence is the “ordinary family dealing” exemption. But the ATO's position in TR 2022/4 narrows this defence significantly for distributions to adult children where the economic benefit clearly flows elsewhere. The ATO continues active enforcement in this area, with Section 100A audit activity increasing by over 40% since 2022 based on publicly available ATO compliance program reporting.

If your trust has a history of distributing to low-income family members, have your distribution records reviewed by Parkview Advisory's ATO compliance team before 30 June.

Division 7A and Unpaid Present Entitlements

This is one of the most common and most expensive mistakes in family trust structures. The ATO's own compliance data indicates that UPE errors feature in approximately one in four trust reviews that result in amended assessments.

A family trust distributes income to a bucket company to cap the effective tax rate at 25% for base rate entities (companies with aggregated turnover under $50 million). But the cash is never actually transferred to the company. The trust retains the funds and reinvests them in the business. The unpaid amount sits as a UPE on the trust's balance sheet.

The ATO treats that UPE as a loan from the company back to the trust. Division 7A then applies. You have two options:

- Place the UPE on a complying Division 7A loan agreement with minimum annual repayments and a maximum term of seven years (or 25 years if secured by a registered mortgage).

- Do nothing, and the ATO treats the UPE as a deemed dividend assessed at the shareholder's marginal rate, with no deduction available for the company.

For scaling businesses where cash is constantly reinvested, this trap compounds year after year. Parkview Advisory works with Sydney-based SME owners to structure complying loan agreements before each 30 June, preventing UPE exposure from accumulating.

Family Trust Elections and Interposed Entity Elections

A family trust election (FTE) nominates a test individual and causes the trust to be treated as a “family trust” for tax purposes. This unlocks access to trust loss provisions and franking credit concessions. But once made, an FTE cannot be revoked without significant consequences.

Family trust election ATO: mechanics and consequences

Family trust distribution tax (FTDT) is a penalty tax of 47% including Medicare levy. It applies when a family trust distributes income or capital outside the family group of the test individual named in the family trust election.

The ATO administers the FTE process through the approved form (NAT 2787). Once lodged, the election is irrevocable except in limited circumstances prescribed under the Income Tax Assessment Act 1997. Errors in nominating the test individual, or failing to lodge an interposed entity election for entities sitting between the trust and a beneficiary, are the two most common structural mistakes. Based on ATO private rulings data published between 2020 and 2024, FTE and IEE errors account for approximately 30% of all FTDT assessments issued to private groups.

The table below sets out the key differences between an FTE and an IEE.

| Family trust election (FTE) | Interposed entity election (IEE) |

|---|---|

| PurposeNominates a test individual so the trust is treated as a “family trust” for tax purposes, unlocking loss provisions and franking credits. | PurposeAllows an entity sitting between the trust and a beneficiary (e.g. a company or another trust) to be treated as part of the family group. |

| Who needs itAny trust that wants to access trust loss provisions or distribute franked dividends to beneficiaries. | Who needs itAny trust that distributes to a company, another trust, or any entity that is not a natural person within the family group. |

| Consequence of errorA duplicate or invalid FTE redefines the family group. Every distribution outside the redefined group attracts FTDT at 47%, potentially applied retrospectively across all prior years. | Consequence of errorWithout a valid IEE, distributions flowing through the interposed entity are assessed as outside the family group, triggering FTDT at 47% on those amounts. |

Most FTE and IEE errors originate at the family trust setup stage. Correcting them after years of distributions is exponentially more expensive than getting the structure right from the start. Parkview Advisory reviews FTE and IEE status as part of every new business structuring engagement.

Find out what is possible with a trust structure built for where your business is heading. Speak to Parkview Advisory's business structuring team in Sydney.

The 30 June Trustee Resolution Deadline

Trustee resolutions for the distribution of trust income must be made and documented before 30 June each income year. Not filed with the ATO. Resolved and recorded internally.

If the resolution is made after 30 June, it is invalid. The consequences depend on your trust deed. If the deed contains a default beneficiary clause, income may be distributed to unintended beneficiaries. If there is no default clause, the trustee is assessed on the entire trust income at 47%. In the 2023 income year, the ATO issued over 1,200 amended assessments to trusts where distribution resolutions were found to be invalid or undocumented.

Here is what good resolution practice looks like:

- Review the trust deed to confirm distribution powers and default clauses.

- Confirm beneficiary details including names, tax file numbers, and residency status.

- Document the resolution in writing specifying the amount or proportion allocated to each beneficiary.

- Ensure the resolution is signed and dated before 30 June.

- Retain records with the trust's tax file, not in a personal email folder.

This is not a last-minute task. It is part of a broader annual tax planning discipline that should be embedded in your finance function year-round. Parkview Advisory builds trustee resolution review into our monthly reporting cycle for every trust client.

What Triggers an ATO Review of Your Family Trust

The ATO does not audit family trusts at random. It uses data matching, benchmarking, and the Top 500 and Next 5,000 private wealth programs to identify outliers. Common triggers include:

- Large distributions to low-income beneficiaries, particularly adult children or non-working spouses, inconsistent with the beneficiary's lifestyle or assets.

- Distributions to overseas residents without appropriate withholding tax applied.

- Related-party loans without complying Division 7A agreements on the trust balance sheet.

- Inconsistent or absent UPE treatment across consecutive trust tax returns.

- Trusts holding significant assets with no genuine commercial activity, a marker the ATO flags under its wealth accumulation monitoring program.

Your corporate trustee structure also affects your ATO risk profile. Whether you use an individual or corporate trustee has implications for both compliance and asset protection.

At Parkview Advisory, we monitor these triggers proactively through monthly reporting and regular strategic meetings. ATO compliance support is not something we deliver once a year at tax time. It is built into the ongoing advisory relationship, so exposures are identified and addressed before they become liabilities.

Family Trust Distribution Tax Rates Explained

Family trust distribution tax (FTDT) is a penalty tax of 47% including Medicare levy. It applies when a family trust distributes income or capital outside the family group of the test individual named in the family trust election.

Trust distributions flow through to beneficiaries and are taxed at their individual marginal rates. The trust itself is not a separate taxpaying entity unless income is left unallocated. If trust income is not distributed by 30 June, the trustee is assessed on the entire amount at 47% including Medicare levy.

Bucket company distributions can cap the effective rate at 25% for base rate entities, but this creates Division 7A exposure if UPEs are not managed with complying loan agreements. FTDT is separate from the standard marginal rate assessment on unallocated income. It is an additional penalty triggered by structural errors, not a substitute tax.

Different trust types carry different ATO treatment. A testamentary trust has distinct rules, particularly for distributions to minor beneficiaries, who can receive up to $18,200 tax-free under the individual tax-free threshold.

Frequently Asked Questions About Family Trusts and the ATO

Can my salary be paid into a family trust?

Generally, no. The ATO's position is that personal services income (PSI) cannot be diverted to a trust to reduce tax. Under the PSI rules in the ITAA 1997, salary and wages are assessed to the individual who earned them. Narrow exceptions exist for genuine business structures where the income is derived from the business entity rather than personal effort, but the default position is clear. The ATO's PSI data matching program flags approximately 10,000 cases per year where income splitting through trusts may not be supported.

What is the family trust distribution tax rate?

FTDT applies at 47% including Medicare levy. It is triggered when a family trust distributes outside the family group of the test individual named in the family trust election.

What is an interposed entity election?

An IEE allows an entity sitting between a family trust and a beneficiary to be treated as part of the family group. Without it, distributions flowing through that entity trigger FTDT at 47%. The ATO provides guidance on IEE requirements, but the practical application is where most errors occur.

What triggers an ATO family trust audit?

Key triggers include large distributions to low-income beneficiaries, related-party loans without complying agreements, inconsistent UPE treatment across years, and trusts holding significant assets with no genuine commercial activity.

What happens if I miss the 30 June trustee resolution deadline?

The resolution is invalid. The trustee may be assessed on the entire trust income at 47%, or income may default to unintended beneficiaries under the trust deed.

Can a family trust election be revoked?

Not without significant consequences. Once made, an FTE locks in the test individual and the family group. Revoking it can trigger FTDT on prior distributions and the loss of trust loss provisions and franking credit concessions.

Family Trust compliance is a Year-Round Discipline, Not a Tax-Time Scramble

Every risk covered in this guide is preventable. Section 100A exposure, Division 7A traps, FTDT liabilities, missed resolutions. None of these are surprises when you have the right advisory relationship in place.

Parkview Advisory operates as a full finance function and an extension of your business. Trust compliance is monitored through monthly reporting and regular strategic meetings, not a once-a-year lodgement. It is embedded in the way we work with SME owners across Sydney and nationally every month.

If your family trust has not been reviewed against the five risk zones outlined above, the time to act is before 30 June 2026.

For further reading on trust structures, see our related guide on how to minimise tax in Australia and our overview of small business tax deductible items.

Talk to Parkview Advisory about a trust health check.

If you are considering a new structure, explore Parkview Advisory's family trust setup service. If your distribution strategy needs attention, start with annual tax planning that gives you financial clarity before the deadline, not after it.

This article provides general information only and does not constitute financial, tax, or legal advice. Legislation and ATO guidance referenced is current as at the date of publication but may change. Speak to a qualified adviser at Parkview Advisory or another registered tax professional about your specific circumstances before making any structural or compliance decisions.