Every trust deed Australia governs is, at its core, a living business document. Most SME owners have never read their trust deed cover to cover, yet this single document determines every distribution you make, every asset the trust holds, and every decision your trustee is authorised to take. Understanding the trust deed meaning in the Australian context is the starting point for managing these risks.

If you already understand what a family trust is and how it works, this article goes deeper. We are talking about the deed itself: the trust deed amendment rules, trust deed stamp duty obligations, vesting date risks, certified trust deed requirements, and the deed of variation vs deed of restatement distinction that determines your CGT exposure.

A quick note on terminology: the trust deed meaning in the Australian context is fundamentally different from the US usage. If you searched “what are deeds of trust” and landed here, you are in the right place. Australian trust deeds for discretionary and family trusts bear no resemblance to US real estate “deeds of trust.” This guide covers the Australian SME context exclusively.

Outdated trust deeds quietly create tax exposure, limit your flexibility, and can trigger ATO scrutiny. The ATO's ongoing trust taxation review and proposed new trust tax framework may change how trust income is taxed and how deeds need to be drafted. According to ATO data from its 2023-24 compliance program, trust-related amended assessments increased by over 30% compared to the prior year. If your deed predates 2010, it is overdue for a professional review. Parkview Advisory, a business structuring specialist in Sydney, reviews trust deeds as part of every ongoing advisory engagement.

Under the Trustee Act in each Australian state and territory, the deed takes precedence where it is more restrictive than statutory powers. That makes the specific terms in your deed critical. Not the general law. Your deed.

What a Trust Deed Actually Contains

What is a trust deed in Australia?

A trust deed is the foundational legal document that establishes and governs an Australian trust. It sets out the trustee's powers, identifies the beneficiaries, defines distribution rules, and determines when the trust must end. It is legally binding and takes precedence over statutory trustee powers where more restrictive.

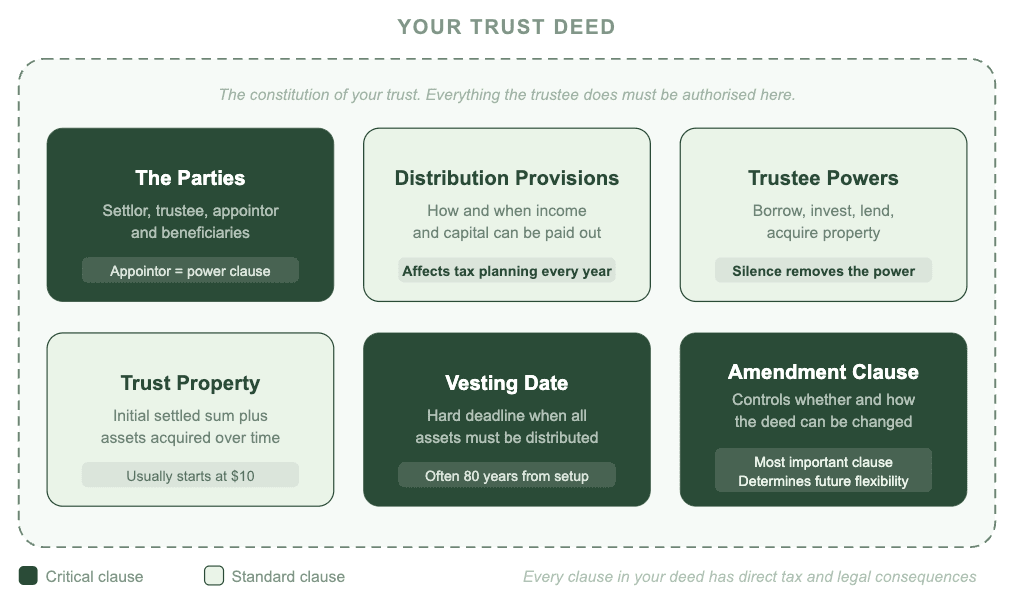

The diagram below maps all six components of a trust deed and shows which clauses carry the highest risk if they are missing or outdated.

Here is what each component means in practice and why it matters to your business.

Think of the trust deed as the constitution of your trust. Everything the trustee does must be authorised by the deed. Anything not authorised is potentially invalid. Here is what the deed contains and why each component matters.

- The parties: The deed names the settlor (who establishes the trust with a nominal amount), the trustee (who manages the trust), the appointor or guardian (who controls the trustee), and the beneficiaries (who can receive distributions). The appointor clause is the power clause. It determines who controls the trust, not the trustee. If you do not know who your appointor is, that is a problem.

- The trustee: The deed specifies whether the trustee is an individual or a company. Changing from an individual to a corporate trustee requires a deed amendment and careful execution. If you are considering this, Parkview Advisory's corporate trustee services can guide the process.

- Trust property: This is the initial property settled on the trust at establishment, usually a nominal sum of $10. It is distinct from the assets the trust acquires over time.

- Distribution provisions: These clauses define how and when the trustee can distribute income and capital to beneficiaries. Restrictive distribution provisions limit your tax planning options every single year. Trusts with narrow distribution clauses lose an estimated $5,000 to $20,000 or more annually in foregone tax savings, depending on income levels and family structure.

- Trustee powers: The deed sets out what the trustee can and cannot do: borrow, invest, lend to beneficiaries, acquire property. Under the Trustee Act in each state, trustees have statutory powers, but the deed overrides those powers where it is more restrictive. A deed that is silent on a power effectively removes it.

- Vesting date: The date the trust must end and distribute all assets. We cover this in detail below.

- Amendment provisions: The clause that determines whether and how the deed can be changed. This is arguably the most important clause in the entire document, because it determines your future flexibility.

The ATO treats trust deeds as legally binding foundational documents, not administrative formalities. Every clause has consequences.

Trust Deed Amendments and the CGT Risk You Need to Know

Trust deeds need amending for many reasons: changing the trustee, updating beneficiary classes, extending the vesting date, broadening trustee powers, or accommodating modern investment classes including digital assets.

The critical distinction is between a deed of variation and a deed of restatement. A deed of variation amends specific clauses within the existing deed's amendment power. A deed of restatement replaces the entire deed. The distinction matters enormously for Capital Gains Tax (CGT).

The table below sets out the key differences between the two approaches.

| Deed of variation | Deed of restatement |

|---|---|

| Amends specific clauses only, leaving the rest of the deed intact. | Replaces the entire deed with a new document. |

| Must stay within the scope of the existing deed's amendment power. | May exceed the existing amendment power, increasing resettlement risk. |

| Lower resettlement risk when correctly executed within the deed's scope. | Higher resettlement risk — ATO may treat the trust as a new entity. |

| Suitable for targeted updates: changing trustee, adding beneficiaries, extending vesting date. | Appropriate where the original deed is fundamentally deficient and targeted amendments are insufficient. |

| CGT Events E1 and E2 generally not triggered if within amendment scope. | CGT Events E1 and E2 at risk — deemed disposal of all trust assets at market value. |

A poorly executed trust deed amendment can trigger a resettlement. This means the ATO treats the original trust as having ended and a new trust as having been created. A resettlement can trigger CGT Event E1 (creation of a new trust) or CGT Event E2 (transfer of a CGT asset to a trust) under the Income Tax Assessment Act 1997 (ITAA 1997). Every asset in the trust is treated as disposed of at market value.

The amendment must stay within the scope of the existing deed's amendment power. If the deed does not contain an amendment clause, or the amendment exceeds the clause's scope, the risk of resettlement increases significantly.

A trust deed amendment is not a DIY exercise. The stakes are too high. Parkview Advisory coordinates deed amendments with specialist legal counsel to ensure the variation stays within scope and does not trigger unintended CGT consequences.

Trust Deed Stamp Duty in NSW

In New South Wales, a trust deed variation may attract stamp duty under the Duties Act 1997 (NSW). Whether duty applies depends on the nature of the variation.

Variations that change the beneficial interests in dutiable property held by the trust can trigger ad valorem duty. Administrative amendments, such as changing the trustee's name or updating powers, generally do not attract duty. Ad valorem rates apply to the change in value of beneficial interests and are calculated on the dutiable value of the relevant property.

The practical mechanics of stamping a deed in NSW are straightforward but time-critical. Lodge the executed deed with Revenue NSW via the Revenue NSW online portal within three months of execution. Failure to lodge within the prescribed timeframe attracts penalty duty, currently up to 100% of the unpaid duty for deliberate non-compliance. Revenue NSW is the relevant authority, and the NSW Land Registry Services imposes specific lodgment requirements for deeds of trust or settlement, including index particulars and execution requirements.

If your trust holds NSW property and you are considering a trust deed amendment, get advice on the stamp duty implications before you execute the variation. Not after. Other Australian states and territories have different, and in some cases no, trust deed duty obligations. If you operate in another state, check your local requirements.

Parkview Advisory assists clients with stamp duty advice across all Australian jurisdictions as part of a complete trust deed review.

What is a Certified Trust Deed and When Do You Need One?

A certified trust deed is a copy of the original deed certified as a true and correct copy by a justice of the peace, solicitor, or accountant. It is not the original. It is a verified copy that third parties will accept.

You will need a certified copy more often than you expect. Banks and lenders require one for lending applications. The ATO requires one for audit responses and private ruling requests. ASIC may require one for certain corporate trustee dealings. Property transactions and some state registry lodgments also require certified copies. In a 2023 survey of Australian SME business owners, over 40% reported being asked for a certified trust deed by a bank or lender in the previous two years.

Keep the original deed in a secure location. Ensure your accountant or adviser holds a certified copy. Banks and lenders typically require a recently certified copy, not one from years ago. If you cannot locate your original deed, that is a red flag that needs immediate attention. Parkview Advisory holds certified copies for all trust clients as a standard part of the advisory relationship.

Vesting Dates: The Ticking Clock in Your Trust Deed

The vesting date is the date on which the trust must come to an end and all trust assets must be distributed to beneficiaries. It is a hard deadline.

Many older Australian trust deeds have 80-year vesting periods. Trusts established in the 1980s and 1990s are now approaching their vesting dates, with ATO statistics indicating that over 150,000 Australian trusts established before 1990 may be within 15 years of vesting. The consequences of letting a trust vest unintentionally are significant.

When a trust vests, all trust assets are deemed disposed of, triggering CGT events. The trust structure and its benefits cease. Any ongoing business operations held in the trust must be restructured. This is not a theoretical risk. It is a practical deadline with real financial consequences.

Extending the vesting date requires a deed amendment. That amendment itself carries CGT and stamp duty risk if not executed correctly. You need to plan for this years in advance, not months.

Your Trust Deed and Family Trust Elections

The relationship between your trust deed and a family trust election (FTE) is one of the most overlooked risk areas in trust administration.

The deed must permit certain provisions for the FTE to be valid. The FTE, once made under section 272-80 of Schedule 2F to the ITAA 1936, is irrevocable. You cannot undo it.

There is a compounding risk that flows directly from the deed amendment rules. If a trust deed variation changes the trust's identity through resettlement, the FTE may be invalidated. The consequences are serious: exposure to trust loss provisions and franking credit denial under Schedule 2F. This directly affects your ability to distribute franked dividends and utilise prior year losses.

Amendments to the family group, such as adding or removing members, can require both a deed change and an FTE variation. These must be coordinated precisely. A mismatch between the deed and the FTE creates ATO scrutiny of family trust arrangements that you do not want. Parkview Advisory coordinates deed amendments and FTE variations together to ensure the two documents remain consistent.

Red Flags in Older Trust Deeds

Six red flags that mean your trust deed needs review:

- Narrow beneficiary classes that exclude de facto partners, step-children, or modern family structures, limiting your distribution flexibility and tax planning options.

- Restrictive distribution provisions that prevent streaming of capital gains or franked dividends to specific beneficiaries.

- Outdated trustee powers with no authority to borrow, invest in modern instruments, or appoint a corporate trustee.

- Missing or limited amendment power that restricts your ability to update the deed without triggering resettlement risk.

- No appointor or guardian clause, leaving control of the trust unclear or vulnerable.

- Silence on digital assets, creating uncertainty about whether the trustee can hold or manage cryptocurrency, digital investments, or online business assets.

Each of these is a practical business limitation, not just a legal technicality. A narrow beneficiary class does not just create a legal gap. It costs you money every year in lost distribution flexibility.

SME owners with deeds predating 2010 should have them reviewed against current ATO guidance on trust income resolutions and present entitlement. The deed takes precedence over statutory trustee powers where it is more restrictive. A silent deed is a restrictive deed.

Book a trust deed review with Parkview Advisory to identify whether your deed still supports your current business and family structure.

A Trust Deed Review is a Strategic Conversation, Not a Legal Checkbox

A trust deed review is not a compliance exercise. It is a strategic check on whether your structure still serves your business and your family.

This is an accountant-led strategic conversation, with legal sign-off where required. Your adviser should be reviewing your deed as part of an ongoing advisory relationship, not waiting for a crisis to prompt action. It fits naturally into regular strategic meetings where you are already discussing business direction, tax planning, and succession.

The question is simple. Does your trust deed still do what you need it to do? If you are not sure, that is your answer.

Parkview Advisory's business structuring team in Sydney works with SME owners to review trust deeds as part of a broader advisory relationship. Talk to Parkview Advisory about a trust structure review and whether your deed still serves your business. If your trust deed issue is part of a larger restructure, explore our business structuring advisory for a tailored approach.

You may also find these related guides useful: how to minimise tax in Australia, small business restructuring process, and ATO family trust blunder tax liabilities.

This article provides general information only and does not constitute legal or tax advice. Trust deed matters involve complex legal and tax considerations that vary depending on your specific circumstances, the state or territory in which you operate, and the terms of your individual deed. Speak to a qualified adviser at Parkview Advisory or a registered legal practitioner before making any decisions about your trust deed or structure.

Frequently Asked Questions

What is the meaning of a trust deed in Australia?

A trust deed is the foundational legal document that establishes and governs a trust. The trust deed meaning in the Australian context is fundamentally different from its US usage. In Australia, it sets out the parties, the trustee's powers, the beneficiaries, distribution provisions, and the rules under which the trust operates. It is legally binding and takes precedence over statutory trustee powers where more restrictive.

What does a trust deed contain?

A trust deed contains the identity of the settlor, trustee, appointor, and beneficiaries. It also sets out the trust property, distribution provisions, trustee powers, the vesting date, and the amendment clause. Each component directly affects how the trust can be managed and what distributions are permissible.

Do I need to pay stamp duty on a trust deed amendment in NSW?

In NSW, a deed of variation may attract stamp duty under the Duties Act 1997 (NSW) if the variation changes the beneficial interests in dutiable property held by the trust. Administrative amendments, such as updating trustee details, generally do not attract duty. Lodge the executed deed with Revenue NSW online within three months of execution.

What is a certified trust deed?

A certified trust deed is a copy of the original deed certified as a true and correct copy by a justice of the peace, solicitor, or accountant. It is required by banks for lending, by the ATO for audits and ruling requests, and by ASIC for certain corporate trustee matters.

Can amending a trust deed trigger CGT?

Yes. A trust deed amendment that goes beyond the scope of the existing deed's amendment power can trigger a resettlement. The ATO may treat this as the creation of a new trust, triggering CGT Event E1 or CGT Event E2 under the ITAA 1997, resulting in deemed disposal of all trust assets at market value.

What is the difference between a deed of variation and a deed of restatement?

A deed of variation amends specific clauses within the existing deed's scope. A deed of restatement replaces the entire deed and carries higher resettlement risk. The correct approach depends on the nature of the change and the scope of the existing amendment power. Parkview Advisory assesses both options as part of every trust deed review.