A discretionary trust in Australia is one of the most widely used structures for SME owners managing business income, investment assets, and family wealth. If you have been searching for the difference between a discretionary trust and a family trust, here is the short answer: there is not one. A family trust is a discretionary trust. The two terms describe the same legal structure from different angles.

“Discretionary trust” describes how the structure works: the trust deed gives the trustee absolute discretion to distribute both income and capital among beneficiaries. “Family trust” is simply the colloquial name used when those beneficiaries are family members. As the ATO confirms, a discretionary trust is often set up by a family, and that is where the label comes from.

There is one important distinction. A discretionary trust only becomes a “family trust” in the ATO's eyes when the trustee lodges a Family Trust Election (FTE). Without an FTE, the trust is still a discretionary trust. It just does not unlock certain tax concessions. More on that below.

If you are new to family trusts in Australia, the real comparison SME owners need is not between discretionary and family trusts. It is discretionary vs unit vs hybrid. That is what determines how your structure actually works in practice.

What is a Discretionary Trust

A discretionary trust in Australia is a private legal structure in which the trustee has complete discretion over how income and capital are distributed among beneficiaries each year. There are no fixed entitlements. The trustee decides who receives what, based on each year's circumstances. It is the most common trust structure used by Australian SME owners and family businesses.

Use this when: you want maximum flexibility to distribute income and capital among family members based on each year's circumstances.

A discretionary trust is set up under a trust deed that governs all rules of operation. It is ideal for family businesses, investment holdings, and income-splitting strategies. According to ATO data, there are over 800,000 discretionary trusts operating in Australia, making them the most prevalent trust structure by a significant margin. The key structural parties are:

- Settlor. Provides a nominal initial sum to establish the trust, then has no further role.

- Trustee. Holds the assets, makes distribution decisions, and lodges tax returns.

- Appointor. Holds the power to appoint and remove the trustee. This is the real control mechanism, and the role most SME owners underestimate.

- Beneficiaries. Those who may receive distributions, entirely at the trustee's discretion.

The appointor role matters most. Whoever controls the appointor controls the trust. If you are setting up a discretionary trust for your business, understanding this power dynamic is critical. Parkview Advisory's business structuring team in Sydney spends dedicated time on appointor structure with every new trust client.

Consider a couple running a growing services business with two teenage children. The trustee can distribute income to lower-earning family members each year, adjusting allocations as circumstances change. The potential tax savings from distributing $120,000 among three family members in lower tax brackets rather than to one individual at the top marginal rate can exceed $20,000 annually.

What is a Unit Trust

Use this when: you need fixed, proportional ownership, typically when unrelated parties are investing together and each needs certainty about their entitlement to income and capital.

Beneficiaries in a unit trust hold fixed units, similar to shares in a company. Each unit represents a proportional entitlement to income and capital. The trustee cannot redirect distributions. Entitlements follow unit holdings, making unit trusts more suitable for unrelated business partners or external investors who require certainty of return.

Example scenario: two unrelated business partners each contribute 50% of the capital to purchase a commercial property. Each holds 50 units and receives exactly 50% of rental income. If one partner wants to exit, their units can be transferred or sold, giving clear exit pathways without restructuring the entire trust.

The trade-off is flexibility. A unit trust vs discretionary trust comparison comes down to: certainty for unitholders versus flexibility for the trustee. You cannot have both in the same structure, unless you move to a hybrid.

What is a Hybrid Trust

Use this when: you need elements of both discretionary and unit trust structures, typically in complex situations involving both family members and external investors. A hybrid trust combines fixed-unit and discretionary components in a single trust deed. Some beneficiaries hold fixed units with proportional entitlements. Others sit in the discretionary class, where the trustee retains full flexibility over distributions.

Example scenario: a business owner brings in an external investor who needs a fixed 30% return. The investor holds units representing that entitlement. The owner's family retains discretionary access to the remaining 70%, with the trustee allocating income across family members each year based on their tax positions.

Hybrid trusts are more complex to establish and administer. They suit specific commercial arrangements, not general family use. If your situation does not genuinely require both fixed and flexible elements, a straightforward discretionary or unit trust will serve you better.

Discretionary Trust vs Unit Trust vs Hybrid Trust

This trust structure comparison covers the practical differences that matter for SME owners making a structuring decision.

| Feature | Discretionary trust | Unit trust | Hybrid trust |

|---|---|---|---|

| Distribution control | Trustee has absolute discretion | Fixed by unit holdings | Mixed: fixed for unitholders, discretionary for others |

| Income splitting | Yes, full flexibility each year | No, income follows units | Partial, only on the discretionary component |

| CGT discount | Yes, 50% for assets held 12+ months | Yes, same eligibility | Yes, same eligibility |

| Asset protection | Strong, no fixed entitlements | Weaker, unitholders have identifiable interests | Mixed, depends on component |

| Setup complexity | Standard | Standard | Higher, requires careful drafting |

| Typical use case | Family business, investment holdings | Unrelated co-investors, property syndicates | External investor plus family flexibility |

Choose a discretionary trust if you want full flexibility to allocate income and capital among family members each year.

Choose a unit trust if all parties need fixed, proportional entitlements and clear exit pathways.

Choose a hybrid trust if your arrangement genuinely requires both fixed equity for some parties and discretionary distributions for others.

If you are still deciding between entity types, start with our sole trader vs company comparison.

Tax Implications for Australian Trusts

The trustee of a discretionary trust can allocate income to beneficiaries in lower tax brackets each year, reducing the overall family tax burden without changing the trust's structure. This is one of the most powerful tools available to SME owners, and it is the primary reason over 800,000 Australian families use discretionary trusts. Unit trusts do not offer this flexibility as income follows unit holdings regardless of each beneficiary's tax position.

- The 50% CGT discount: Trust-held assets held for more than 12 months are eligible for the 50% CGT discount when distributed to individual beneficiaries. This applies equally to discretionary, unit, and hybrid trusts.

- Trust loss quarantine. This is a critical disadvantage. Losses are trapped inside the trust and cannot be distributed to beneficiaries or offset against personal income. This applies to all three trust types. If your structure is likely to generate losses in early years, a trust may not be the right vehicle. A sole trader or partnership structure allows losses to flow through to your personal return.

- Family Trust Election. Lodging an FTE with the ATO unlocks access to trust loss concessions and franking credit streaming, but it locks the trust into a defined “family group.” Distributions outside that group attract tax at the top marginal rate of 47%. Not every discretionary trust needs an FTE. It depends on whether the trust receives franked dividends and whether prior-year losses need to be recouped. Parkview Advisory assesses FTE eligibility for every new trust engagement.

How to Choose the Right Trust Structure

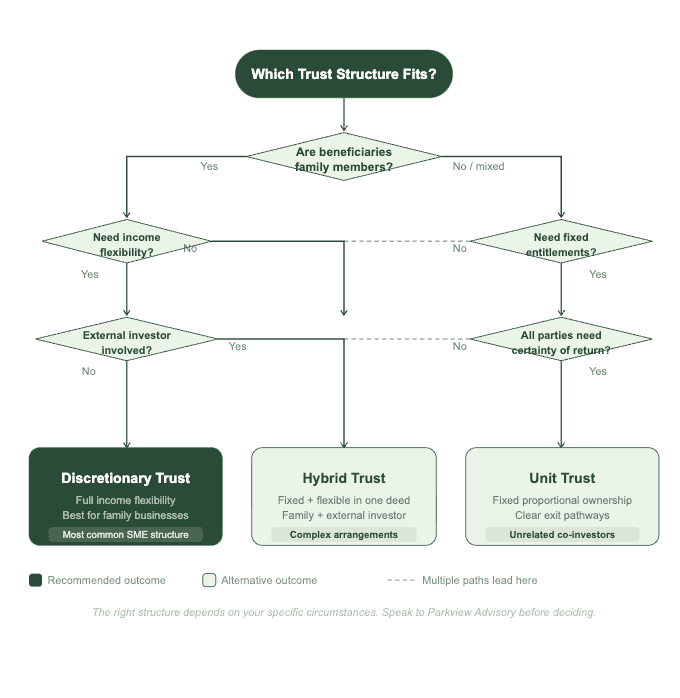

The right type of trust is determined by your commercial circumstances. Start with these questions:

- Who are the beneficiaries? Related family members, or unrelated parties?

- What will the trust hold? Investments, a trading business, or property?

- Do any parties need fixed entitlements? Certainty of return, transferable units, clear exit rights?

- What are the income-splitting opportunities? Consider each beneficiary's marginal tax rate.

- What is the growth trajectory? Will external investors or partners come in later?

The flowchart below turns those five questions into a decision path, follow the branches that match your situation to reach the right structure.

The three scenarios below show what each outcome looks like in practice.

Three scenarios

Scenario 1: Family business owner. You run a consultancy with your spouse and want to split income across family members. A discretionary trust gives you full flexibility. Consider a family trust setup as your starting point.

Scenario 2: Unrelated co-investors. You and a business associate are purchasing a commercial property 50/50. A unit trust gives each party fixed entitlements and a clean exit mechanism.

Scenario 3: Business owner plus external investor. You are bringing in capital from an outside party that requires a guaranteed return, while your family retains flexible access to the remaining profits. A hybrid trust handles both requirements in a single structure.

If you are still weighing trusts against other entity types, explore Parkview Advisory's business structuring services. The right structure is a strategic decision, not a compliance checkbox.

Find out what is possible with a tailored structuring review from Parkview Advisory.

Where Testamentary Trusts Fit In

Everything above applies to inter vivos (lifetime) trusts, established and operated during your lifetime. Testamentary trusts are a distinct category, established through a will and activated only on the death of the will-maker.

The key difference for SME owners: testamentary trusts offer concessional tax treatment for minor beneficiaries (under 18). Income from a testamentary trust is taxed at adult marginal rates rather than the penalty rates that apply to minors receiving income from inter vivos trusts, which are taxed at up to 47% from the first dollar. This makes testamentary trusts a powerful estate planning tool for business owners with dependent children.

Learn more about how a testamentary trust setup fits into your estate planning. You may also find our guides on tax planning strategies and small business capital gains tax concessions useful reading.

Frequently Asked Questions

Is a family trust the same as a discretionary trust?

Yes. A family trust is a discretionary trust where the beneficiaries are family members. The only formal distinction arises when a Family Trust Election is lodged with the ATO, which creates a specific tax designation and restricts distributions to a defined family group.

What is a unit trust?

A unit trust is a structure where beneficiaries hold fixed units representing their proportional entitlement to income and capital. Unlike a discretionary trust, the trustee cannot redirect distributions. Entitlements follow unit holdings.

What is the difference between a unit trust and a discretionary trust?

In a discretionary trust, the trustee decides who receives income and capital each year. In a unit trust, entitlements are fixed by unit holdings. The key trade-off is flexibility versus certainty of return.

What is a hybrid trust?

A hybrid trust combines discretionary and unit trust elements in a single deed. Some beneficiaries hold fixed units while others receive distributions at the trustee's discretion. They suit complex arrangements involving both family members and external investors.

Can a company be a trustee of a discretionary trust?

Yes. Using a corporate trustee is standard practice in Australia. It provides an additional layer of asset protection because the company's liability is limited to the trust assets, shielding the personal assets of the individuals behind it. Parkview Advisory recommends a corporate trustee for most SME trust structures.

How is trust income taxed in Australia?

The trust itself is not taxed if all income is distributed to beneficiaries by 30 June. Each beneficiary pays tax at their individual marginal rate. Any undistributed income is taxed at the top marginal rate of 47%, making full distribution essential in most cases.

When should I choose a company instead of a discretionary trust?

A company structure may be preferable when your business needs to retain earnings at the flat corporate tax rate of 25% (for base rate entities with aggregated turnover under $50 million), rather than distributing them to individual beneficiaries each year.

Companies also suit situations where you need clear equity ownership, share-based employee incentives, or external investment. Trusts cannot issue shares, cannot retain losses to offset future income in the same way, and must generally make distributions by 30 June each year. Our guide on sole trader vs company covers these trade-offs in detail. Parkview Advisory can help you model which structure produces the better outcome for your specific income level and growth plans.

Get the Right Trust Structure for Your Business

The right type of trust is a strategic decision shaped by your beneficiaries, business model, growth plans, and tax position. It is not something to template.

Parkview Advisory operates as a full finance function and an extension of your business. Working with Parkview Advisory's business structuring team in Sydney means your structure evolves as your business does, with monthly reporting and regular strategic meetings built into the relationship.

Talk to Parkview Advisory about setting up the right trust structure for your business.

This article provides general information only and does not constitute financial, tax, or legal advice. Trust structures involve complex considerations that vary by individual circumstance. Speak to a qualified adviser at Parkview Advisory or another registered tax professional before making any structuring decisions.