Holding company meaning: A holding company in Australia is a company whose primary purpose is to own shares in other companies rather than trade or operate a business itself. It holds long-term value and protects assets from operational risk by sitting above the entities that face day-to-day commercial liability. Under the Corporations Act 2001 (Cth), a holding company is defined as a body corporate of which another body corporate is a subsidiary.

A holding company Australia structure typically places a HoldCo above one or more operating companies (OpCos). The legal basis is Corporations Act 2001 (Cth) s9. Section 46 sets out three tests for subsidiary status: the parent controls the composition of the subsidiary's board, holds more than half of the maximum voting power, or holds more than half of the issued share capital.

The more useful question for SME owners is strategic: when does adding a holding company earn its complexity, and when is it unnecessary overhead? This guide is built around that decision, not what a holding company is in theory, but whether one makes sense for your business right now, your tax position, and your exit options.

Holding Company Structure: How It Typically Works

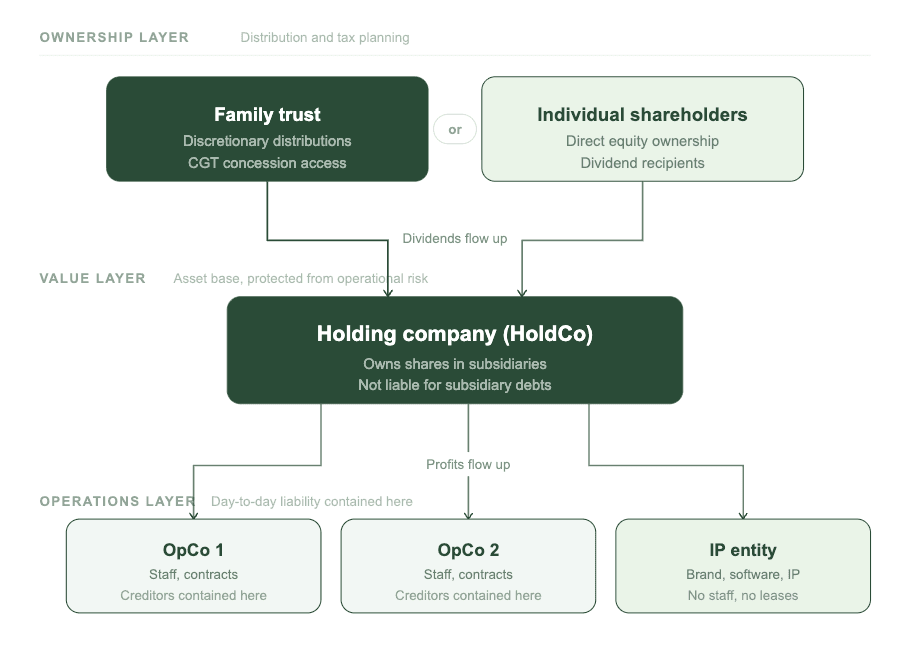

The typical Australian holding company structure follows a clear hierarchy. Family trust or individual shareholders sit at the top. Below them is the holding company (HoldCo). Below HoldCo sit one or more operating companies (OpCos), and sometimes a separate entity holding intellectual property.

The diagram below maps this three-layer hierarchy and shows what each layer does, where value accumulates, and where risk is contained.

Here is what each layer means in practice and why the separation between them matters.

The HoldCo/OpCo distinction is straightforward. HoldCo owns the shares in the group and holds long-term value. OpCos run the day-to-day business: employing staff, holding contracts, signing leases, and facing operational risk. A holding company is a separate legal entity from its subsidiaries, which means it is generally not liable for subsidiary debts. That separation is the structural foundation for asset protection.

Holding company vs family trust: Many SME holding structures sit beneath a family trust rather than using a HoldCo alone. A family trust above the holding company provides flexibility in distributing dividends and accessing CGT concessions, while the HoldCo provides a fixed corporate ownership layer below it. They serve different purposes and often work best in combination. See our guide on how family trusts work in Australia for the trust-specific considerations.

The key point: this is not a one-size structure. The right group structure depends on your commercial objectives, risk profile, and where you are heading. Parkview Advisory's business structuring team in Sydney works with SME owners across all of these configurations.

Four Reasons Scaling SMEs Use Holding Companies

1. Group structures with multiple business lines

If you operate two or more distinct business lines, a holding company gives you a single point of ownership and governance. Each OpCo runs independently with its own contracts, staff, and risk profile. HoldCo sits above, allocating capital and consolidating reporting. According to ASIC data, over 65% of Australian corporate groups with more than two operating entities use a dedicated holding company structure.

This makes sense when your group revenue sits in the $5M to $20M range and you need clear separation between divisions for management accountability, financing, or future divestment. Without HoldCo, cross-entity ownership becomes tangled and difficult to unwind.

2. IP holding and licensing

A SaaS company with valuable software, or a services business with a strong brand, can extract that intellectual property into a separate entity. That entity licenses the IP back to the operating company under a commercial arrangement. Your most valuable intangible asset sits in an entity that does not employ staff, sign leases, or face operational creditors. This structure is worth considering when your IP represents a material portion of total business value.

3. Sale preparation and CGT concession access

Restructuring before a business sale is one of the most common reasons SME owners add a holding company. A clean group structure with IP, goodwill, and operational assets clearly separated increases buyer confidence and reduces due diligence friction. We cover the timing and tax mechanics of pre-sale restructuring in detail below.

4. Risk isolation

Operational businesses carry risk: employee claims, contractual disputes, regulatory exposure. A holding company structure separates the entities that hold long-term value from the entities that face day-to-day liability.

However, this protection is not absolute. Cross-guarantees, personal guarantees, or insolvent trading exposure can pierce the separation in practice. Effective asset protection structuring requires ongoing discipline, not just initial setup.

What is an Ultimate Holding Company?

An ultimate holding company (UHC) is the entity at the very top of a corporate group that is not itself a subsidiary of any other body corporate. The Corporations Act 2001 s9 defines it in exactly those terms.

This is distinct from an immediate holding company, which is the entity directly above a subsidiary in the chain but may itself be owned by another company higher up. In a three-tier group, the middle entity is an immediate holding company. The top entity is the UHC.

The UHC designation carries practical weight. ASIC requires large proprietary companies and public companies within a group to lodge consolidated financial statements, and the UHC determines which entity carries that reporting obligation. As your group grows or considers external investment, the UHC becomes the reference point for related party disclosures and regulatory filings.

Tax Implications of a Holding Company in Australia

The tax position of a holding company in Australia involves several interacting rules. The sections below cover each one. Getting the structure right before you establish it is far cheaper than correcting it after.

Franking credit flow

When a subsidiary pays a franked dividend to its holding company, the franking credits flow with it. HoldCo can then pass those credits to its own shareholders via franked dividends, preserving the tax-paid status of profits through the group. This is one of the clearest advantages of a corporate group structure.

Division 7A risks

Division 7A of the Income Tax Assessment Act 1936 applies to loans, payments, and debt forgiveness between a private company and its shareholders or associates. Intercompany loans within a group must be structured as complying Division 7A loans or as genuine commercial arrangements. Get this wrong and the ATO treats the amount as a deemed unfranked dividend. ATO compliance data indicates Division 7A errors feature in approximately one in four private group audits that result in amended assessments, making it one of the most actively enforced areas in group structures.

Base rate entity rules

A company is taxed at 25% if its aggregated turnover is below $50M and no more than 80% of its assessable income is base rate entity passive income. A holding company that receives only dividends from subsidiaries may breach the 80% passive income threshold, pushing its tax rate to 30%, so this needs modelling before you establish the structure.

Tax consolidation regime

Under Division 705 of the ITAA 1997, eligible corporate groups can elect to be treated as a single entity for income tax purposes. This means intercompany transactions within the consolidated group are effectively ignored for tax, simplifying reporting and eliminating the need to manage Division 7A on intragroup loans. Tax consolidation is typically elected by groups with multiple wholly-owned subsidiaries where the administrative burden of managing separate tax returns outweighs the cost of consolidation.

For most SMEs in the $5M to $20M revenue range, the compliance cost of maintaining a consolidated group may not be justified until the group reaches a certain scale, and Parkview Advisory models this threshold as part of every group structuring engagement.

CGT considerations

Companies do not access the 50% general CGT discount (Division 115, ITAA 1997). This is a critical distinction when comparing a trust-based structure to a corporate holding company for CGT planning. If capital gains are a significant part of your expected returns, a corporate HoldCo may not be the right vehicle. Division 615 rollover relief is available when transferring shares into a holding company structure, allowing deferral of CGT on the transfer.

Small business CGT concessions

The small business CGT concessions (Subdivisions 152-A to 152-E, ITAA 1997) are available to entities with aggregated turnover under $2M or net assets under $6M. A holding company structure can affect whether the active asset test and maximum net asset value test are satisfied. Assets held in a holding company that are not used in an active business may jeopardise eligibility at the point of sale. For a deeper walkthrough, see our small business CGT concessions guide.

The interaction between these rules is where most SME owners need support. Parkview Advisory provides business structure and tax advisory to model the tax position of a holding company against alternative structures before you commit.

Using a holding company to prepare for a business sale

Pre-sale restructuring is one of the most common reasons SME owners add holding company complexity. A clean group structure with IP, goodwill, and operational assets clearly separated increases buyer confidence and reduces due diligence friction. Buyers want to acquire a defined set of assets or shares without inheriting unnecessary risk.

Timing matters. Division 615 rollover relief allows deferral of CGT when transferring shares into a HoldCo, but the small business CGT concessions, including the 15-year exemption and retirement exemption (Subdivisions 152-B and 152-D, ITAA 1997), require a two-year holding period for certain assets. Restructure too late and you miss the concession window.

The best time to restructure is two to three years before a planned exit. This gives you time to satisfy holding period requirements, bed down intercompany arrangements, and present clean financials to prospective buyers.

If you are still deciding on your base structure, our sole trader vs company comparison covers the foundational decision. If you are already operating through a company and thinking about an exit in the next few years, the holding company conversation should be happening now with Parkview Advisory.

When a Holding Company is Worth It (And When It is Not)

The following table summarises when a holding company earns its complexity and when a simpler structure is the better fit.

| Consider a holding company | Probably not worth it |

|---|---|

| You operate multiple business lines or entities under separate companies. | You run a single operating business with low liability risk. |

| You hold significant IP or goodwill worth protecting from operational risk. | Your revenue is under $1M to $2M and ASIC fees, accounting, and admin overhead outweigh the benefit. |

| You are planning a business sale or succession event within two to five years. | You have no exit or succession plan on the horizon. |

| Your business carries material operational risk through staff, contracts, or public-facing liability. | The complexity would outpace your current advisory support. |

| Your group revenue exceeds $2M to $5M and the cost of the structure is proportionate to the benefit. | A trust-only structure already meets your asset protection and distribution objectives. |

A holding company means additional ASIC registration and annual review fees (currently $310 per year for a small proprietary company), separate financial statements, potentially an additional tax return, and ongoing advisory support to manage intercompany transactions. This is not a structure you set up and forget. If you are weighing up whether a holding company fits your situation, talk to Parkview Advisory's structuring team.

Holding Company Examples in Practice

Multi-site services business

A facilities management company operates three locations, each through its own OpCo. A single HoldCo owns all three, holding the brand and IP centrally. A family trust sits above HoldCo. Each OpCo carries its own staff contracts and leases. If one location faces a claim, the other two are structurally insulated.

IP licensing arrangement

A SaaS business extracts its core software IP into a separate entity owned by HoldCo. That entity licenses the software back to the operating company under a commercial licensing agreement. The IP sits in an entity with no employees, no leases, and no operational creditors.

Family group with diverse investments

A family HoldCo owns shares in an active trading business and a separate property investment company. The family trust above HoldCo distributes dividends according to each year's circumstances. The group structure keeps active business risk separate from the investment portfolio.

These holding company examples reflect common Australian patterns. The specifics of your structure will depend on your commercial objectives, risk profile, and tax position.

Getting the structure right from the start

A holding company is a tool, not a status symbol. The question is always whether the structure earns its complexity for your specific situation.

That decision benefits from strategic advisory support: not just legal setup, but ongoing tax, reporting, and commercial guidance that evolves as your business does. Parkview Advisory operates as a full finance function and extension of your business, with monthly reporting and regular strategic meetings built into every engagement.

For further reading, see our guides on ATO family trust blunder tax liabilities, how to minimise tax in Australia, and small business restructuring process.

If your primary concern is the tax position, get tax-led structure advice tailored to your group and your goals.

This article provides general information only and does not constitute financial, tax, or legal advice. Legislative references are current as at the date of publication and may change. Speak to a qualified adviser at Parkview Advisory or another registered tax professional about your specific circumstances before making any structuring decisions.